Survey Says: Personalize The Consumer Experience

According to IABM’s recently released Supply Trends Survey, year-on-year sales in the broadcast and media technology market grew by 1.2 percent in December 2017. But while sales improved slightly, profit growth continued to slow, running at 75.9 percent of the December 2016 level.

So what is going on and what is the way forward?

The continuing shift in buyers’ preferences for software running in generic IT technology, their increased concern for efficiency and a highly competitive market are all continuing to exert pressure on selling prices, with margins reducing despite vendors now decreasing expenditure on R&D, recruitment, sales, marketing and shows.

As broadcasters and media companies increasingly move to software-based, Opex business models, it’s perhaps not surprising that equipment vendors’ profitability has taken a hit — especially as they still need to support legacy hardware-based systems.

But as their R&D investments in software-led technology come to fruition and their reliance on large one-off deals transitions to the more regular, smaller payments of the new Opex model, vendors that have successfully weathered the transition should begin to improve their profitability.

This transition to software (including the cloud) is well underway, though according to the IABM Supply Trends Survey, hardware remains the primary source of both revenues and profits for most suppliers. However, some respondents who said their primary source of revenues is hardware also said that their primary source of profits is now software, which generally carries higher margins than hardware.

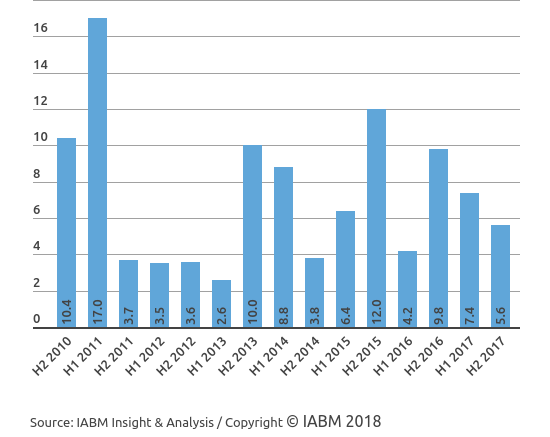

Unsurprisingly given the report’s findings on profitability, the IABM confidence ratio, which reflects business sentiment looking forward for the next year, declined from a fairly robust 7.4 mid-2017 to a less optimistic 5.6 in December 2017; this is relatively low by historical standards.

It’s not just the technology buyers’ business models that are changing, of course; they also have to stay ahead of their customers’ demand for the continuous delivery of new media content as well as a seamless experience on different devices and platforms.

This has required them to revolutionize their workflows to increase speed and eliminate inefficiencies. With SMPTE ST 2110 now published and many companies planning or beginning the move to all-IP signal flows and the cloud, they increasingly have the tools at their disposal to do so — as well as a large pool of media technology vendors keen and able to supply them.

Speed and efficiency alone are not enough, however. Media companies have started investing in personalizing the consumer experience to stand out in a crowded market for content. AI and cloud technology are the tools to analyze and process big data to provide recommendations. Unsurprisingly, recent IABM data shows that the take-up of AI to use data insights intelligently and improve workflows is experiencing a sharp increase in broadcast and media companies, with vendors racing to support them with AI-powered technology.

We are also seeing unprecedented consolidation and convergence between content and distribution by established media companies looking for greater scale to counter the major new online media players.

This reduces overall technology spending simply because as companies merge, they consolidate their operations too — meaning that the number of potential customers is reducing. Greater scale also gives them better bargaining power. The result is that we now have several thousand technology suppliers — many of them right here at NAB Show — chasing business from a diminishing number of customers.

This inevitably puts pressure on prices and reduces profitability for vendors, so more consolidation on the supply side such as the recent acquisition of SAM by Grass Valley, a Belden company, is inevitable. Larger players also will continue to buy-in innovation by acquiring smaller, more agile vendors with specialist applications.

What does this mean for the future of our industry? In the long term, media technology spending will continue to grow as traditional end-user broadcasters try to keep up with the volatile nature of online video. 2017 saw a record number of TV productions; the overall market continues to expand.

Media technology vendors can take advantage of this by supplying users with products that address their business challenges in the transition to a multiplatform world. Product excellence, support and interoperability will be important factors in determining their survival through this unprecedented change.